Global Hotel AI Market Report · April 2026

The global hotel industry has transitioned from a 'recovery cycle' to an 'efficiency competition cycle.' 386,000 rated hotels worldwide; 277,700 at 3-star and above; 70%+ still use manual pricing; AI pricing offers 8–15% net profit uplift. In-depth analysis across 13 countries and regions.

InsightBridge Global Intelligence · Market Report · April 2026

Executive Summary

The global hotel industry has transitioned from a "recovery cycle" to an "efficiency competition cycle." Post-pandemic revenge travel has normalized; hotels can no longer rely on rate increases and occupancy recovery alone. They must confront structural challenges — rising labor costs, persistent staffing shortages, high distribution costs, fragmented guest experiences, and siloed data systems. AI is emerging as the critical infrastructure for the next phase of competitive differentiation.

Key Market Indicators

- 386,000 — Total global rated hotels (GARD Database)

- 277,700 — 3-star and above (~72% of total supply)

- 70%+ — Hotels still using manual pricing (CBRE / STR)

- 8–15% — Potential AI pricing uplift in net profit (PwC)

Global 3★+ Hotel Distribution by Region

- USA: ~5.7M rooms

- China: ~3.8M rooms

- Europe: ~4.5M rooms

- SE Asia: ~1.2M rooms

- Middle East: ~693K rooms

- HK / Macau / Singapore: ~209K rooms

Section II — Critical Pain Points Across the Global Hotel Industry

The hotel industry faces compounding structural pressures. These are not cyclical fluctuations but long-term challenges requiring systemic technological intervention.

1. Labor Shortage & Rising Costs

Post-pandemic workforce shortages persist globally, with rising wages, high turnover, and training costs compressing margins.

2. Outdated Revenue Management

Over 70% of upscale hotels still rely on manual pricing, unable to integrate real-time demand signals from flights, conventions, competitor pricing, and OTA conversion data.

3. Fragmented Guest Experience

Guest interactions span official websites, OTAs, social media, WeChat, email, front desk, and loyalty systems. Siloed data prevents unified customer profiles.

4. Energy & Operational Cost Burden

Hotels are high-energy assets; HVAC, lighting, hot water, laundry, kitchen, and public area systems drive significant operational costs.

Section III — Four Defining Trends in Hotel AI Adoption

Trend 1 — From Chatbot to Operational Brain

AI is penetrating from front-desk service into core operations: revenue management, guest profiling, energy optimization, procurement, scheduling, marketing, and reputation management.

Trend 2 — AI Lands First in High-Value, High-Cost Markets

Markets with high labor costs and mature digital infrastructure — US, UK, Germany, Singapore, Hong Kong, Macau, UAE, Saudi Arabia — generate faster ROI on AI investment.

Trend 3 — Deep Integration with Core Hotel Systems

AI must integrate deeply with PMS, CRM, POS, OTA APIs, door lock systems, and payment platforms — otherwise it remains superficial.

Trend 4 — Efficiency Gains Confirmed; Revenue Uplift Still Emerging

Cost-reduction value is well-established. Revenue-side uplift — precision pricing, membership conversion — requires deep integration with hotel data and channel strategy, and remains in accelerated validation.

Section IV — In-Depth Country & Regional Analysis

| Country / Region | Market Profile | Primary Pain Points | AI Opportunity | AI Maturity |

|---|---|---|---|---|

| 🇦🇪 UAE | ~218,000+ rooms; Dubai high-density luxury | Intense competition, diverse clientele, high operating costs | Luxury guest profiling, dynamic pricing, energy automation | Very High |

| 🇸🇦 Saudi Arabia | ~475,970 licensed rooms; rapid Vision 2030 expansion | Talent gap, Hajj peaks, massive new supply | City-level demand prediction, operational automation, smart tourism platforms | High Growth |

| 🇺🇸 USA | Largest global market; ~5.7M rooms | Labor costs, brand standardization, distribution costs | Revenue management, automated check-in, marketing automation | Very High |

| 🇨🇳 China | 6,000+ rated hotels; OTA-driven market | Chain consolidation, thin margins, OTA dependency | Dynamic pricing, private-domain CRM, smart concierge, review analytics | Mid-High |

| 🇲🇴 Macau | 146 hotels, 43,044 rooms; casino-resort driven | Gaming tourism volatility, integrated resort ops | High-value guest ID, cross-venue recommendation, energy | High |

| 🇭🇰 Hong Kong | ~320 hotels, 92,907 rooms | Expensive labor, limited space, intl recovery | Multilingual AI concierge, RevMgmt, business traveler profiling | High |

| 🇸🇬 Singapore | ~73,000+ rooms; MICE hub | High labor costs, strong MICE demand | Premium service automation, MICE forecasting, guest intelligence | High |

| 🇬🇧 UK | Major European market; London luxury rising | Labor, energy costs, new supply pressure | AI efficiency, upselling, customer segmentation | High |

| 🇩🇪 Germany | ~12,000 accommodation establishments | Labor shortages, uneven business travel | MICE forecasting, operational automation, energy | Mid-High |

| 🇹🇭 Thailand | ~700,000 rooms; tourism-dependent | Extreme seasonality, service labor pressure | Multilingual AI, seasonal demand prediction, review analytics | Mid-High |

| 🇲🇾 Malaysia | KL: ~38,631 rooms in 3–5★ | New supply competition, price pressure | Dynamic pricing, OTA ad optimization, MICE | Mid |

| 🇦🇹 Austria | Record overnight stays; tourism-dependent | Seasonality, ski-resort costs, energy | Seasonal pricing AI, energy mgmt, repeat-guest optimization | Mid-High |

| 🇨🇾 Cyprus | Growing resort tourism revenue | Strong seasonality, overseas source dependency | Seasonal forecasting, international marketing AI, guest service | Mid |

"The competition is no longer about who has more rooms — it's about who operates them with better intelligence."

— InsightBridge Global Intelligence Analysis · April 2026

Section V — Our Perspective: The Next Three Years

Over the next three years, the defining competitive axis in global hospitality will shift from "who has more rooms" to "who operates them with superior intelligence." Hotels rated 3-star and above represent the core addressable market for AI solutions — they possess sufficient operational complexity and data density, while facing the budget pressures and efficiency demands that make AI adoption compelling.

AI will not strip hotels of their human touch. On the contrary, AI's true role is to liberate staff from repetitive tasks and return them to high-value service moments. The most successful hotels of the future will not be fully unmanned — they will be a new model where "AI handles efficiency; people deliver experience."

Regional Strategic Outlook

- Middle East — Rapid build-out: smart tourism, guest AI, city-level platforms

- Asia Pacific — Complex & diverse: smart concierge, RevMgmt, CRM

- United States — Cost-driven mature: automation, RevMgmt, marketing AI

- Europe — Energy AI, scheduling, ESG compliance

- Island / Resort — Seasonal pricing, energy, forecast

References

- GARD Global Accommodation Research Database

- PwC Middle East — AI in Tourism and Hospitality 2025

- Macao DSEC — Tourism and Hotel Statistics 2024

- CBRE Hong Kong — Hotel market supply data, 2024

- Saudi Tourism Authority / SPA — Licensed tourism accommodation data, 2024

- Knight Frank — UAE Hospitality Market Review 2024

- CBRE — 2025 Global Hotel Outlook

- CEIC / Destatis — German accommodation statistics

- Singapore Data.gov.sg — Gazetted Hotels statistics

- Cyprus Government — Tourism Statistics 2024

For full report access, demos, or partnership inquiries: tongyin@insightbridge.global · insightbridge.global

Get the InsightBridge Weekly Brief — free in your inbox

One email a week — distilling the hotel, AI, geopolitical, and macro decisions and analysis that actually matter to executives. Completely free. No noise. Unsubscribe anytime.

Discussion (0)

Related reading

2027 AI × Global Hospitality & Tourism Whitepaper — Frontier, Framework, Frontier Markets

InsightBridge Global's 2027 outlook synthesizes fifty-plus original research pieces into an integrated framework spanning three simultaneously reorganizing layers of hospitality: the Agent Layer (demand capture), the Physical Layer (embodied AI and robotics), and the Sovereignty Layer (data localization). Five headline judgments and an 8-participant × 3-horizon strategic matrix.

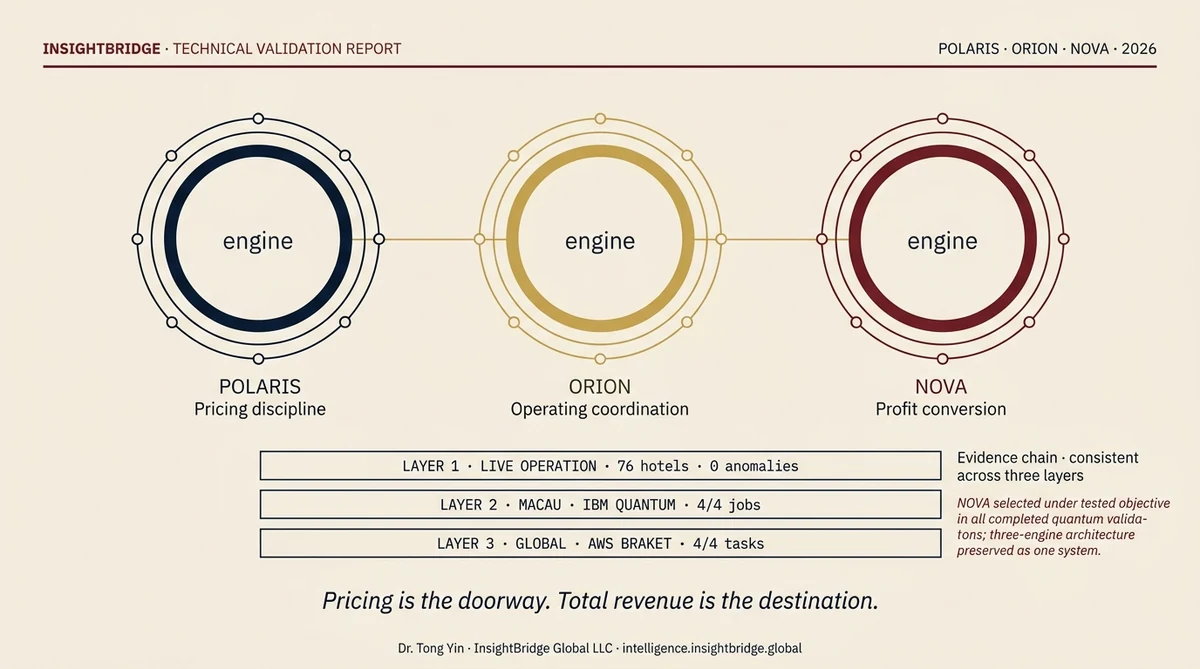

InsightBridge Hotel AI Validation Report — POLARIS · ORION · NOVA Across Three Quantum-Validated Evidence Layers

The platform should not be read as a standalone room-price optimiser. It is a total-revenue optimisation system. Across two completed quantum-validation tracks — Macau on IBM Quantum and a global hotel dataset on AWS Braket — NOVA was selected as the strongest single model in all 8 completed jobs. The full 24-page report (PDF) below.

Why AI Pricing Still Fails Hotels — And What Needs to Change

Most hotel revenue management systems are built on three broken architectural assumptions — stable historical demand, clearly defined competitor sets, OTA-driven pricing signals — all increasingly invalid in 2026. Hotels deploying systems on these outdated assumptions may leave 8–14% of revenue on the table annually. The fix is a three-layer architecture: demand reconstruction from first principles, channel-aware net revenue optimization, and human-in-the-loop learning systems where every override becomes a training signal. As travel discovery migrates from Google to ChatGPT, Gemini and Perplexity, hotels with better data, better content, and adaptive pricing will be recommended ahead of OTAs — intelligence advantage becomes the new distribution moat.